Third-Party Litigation Funding: Why Your Insurance Premiums Keep Rising

Your premiums went up again. You didn’t file a claim. What gives? The answer might surprise you: Third-Party Litigation Funding is quietly transforming business insurance costs across America.

Spotless claims history, responsible risk management, yet your business insurance costs keep climbing. The culprit? It’s likely not anything happening inside your business, but rather a seismic shift in how lawsuits are funded and fought across America.

While everyone’s quick to blame inflation and catastrophic weather events (and yes, they’re part of the equation), there’s a less visible force reshaping your insurance costs that rarely makes headlines: Third-Party Litigation Funding.

Let’s pull back the curtain on what’s really happening, and more importantly, what you can do about it.

What You’re Being Told (And Why It’s Not the Full Story)

“Market conditions.” “Claim severity trends.” “Inflationary pressures.”

These are the explanations that typically arrive with your renewal notice. They’re not wrong, but they’re only chapters in a much longer story.

Think of it like being told your flight is delayed due to “operational issues” — technically true, but hardly the full picture. The missing piece? A dramatic shift in how lawsuits against businesses are financed and fought.

While economic inflation has grabbed headlines, “social inflation” — the rising costs of insurance claims above normal economic inflation — has quietly outpaced it. Between 2017 and 2022, social inflation in the US rose by 5.4% annually, while economic inflation was 3.7%.

And at the heart of this social inflation sits the growing industry of Third-Party Litigation Funding.

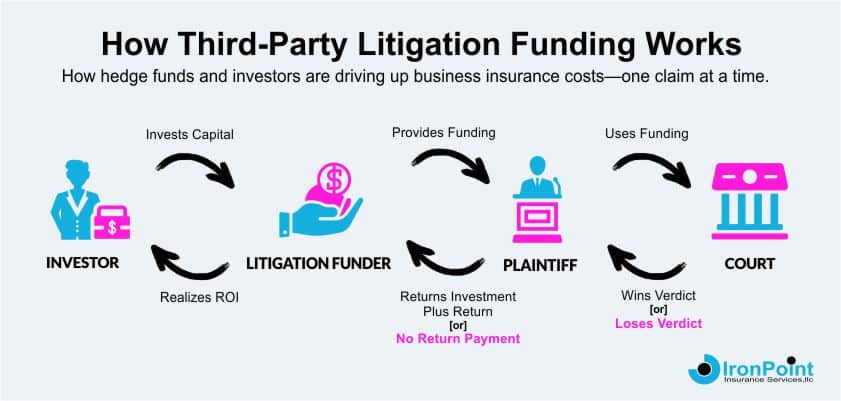

What Is Third-Party Litigation Funding?

Imagine a world where lawsuits are treated like stocks — investments to be bought, sold, and traded based on their potential return.

That world exists today.

Third-Party Litigation Funding occurs when outside investors — typically hedge funds, private equity firms, or specialized funding companies — bankroll lawsuits in exchange for a percentage of any settlement or judgment.

This isn’t your cousin lending you money to hire an attorney. It’s Wall Street meeting the courthouse in a financial arrangement that’s transforming the litigation landscape.

Here’s how it typically unfolds:

- A litigation funder spots a potentially profitable lawsuit (think of them as talent scouts for legal disputes)

- They provide money to cover legal expenses with a crucial caveat: if the case fails, the plaintiff owes nothing

- In exchange, the funder claims a substantial slice of any settlement or judgment — often 30-40% or more

- Unlike your attorney, the funder may have significant influence over litigation strategy, including whether to settle

To see this in action, picture this scenario: A customer slips in your store. In the past, they might have settled quickly for a reasonable amount. Today, with third-party backing, they can afford top expert witnesses, endless depositions, and years of litigation — all while facing zero financial risk themselves.

The result?

Cases that once settled for $50,000 now routinely command $500,000 or more. And your insurance premiums absorb the shock waves.

Why It’s Driving Up Business Insurance Premiums

The litigation funding industry has ballooned from a niche financial strategy to a market juggernaut. According to Research Nester, this market is projected to exceed $50 billion by 2036, up from approximately $17.5 billion in 2024.

That’s not just growth — it’s a fundamental shift in how our legal system operates. And it affects your insurance costs in four critical ways:

1. More Lawsuits Get Greenlit

When plaintiffs needed their own money to pursue lawsuits, many legitimate (but expensive) cases never made it to court. Now, with third-party funding, the financial barriers have disappeared.

It’s like what happened when streaming services made it easier to produce TV shows — suddenly, there’s a lot more content, some good, some questionable, but all of it competing for attention.

2. Settlements Get Supersized

When you’re playing with house money, why fold early?

Plaintiffs backed by litigation funders can afford to reject reasonable settlement offers and hold out for bigger payouts. This has fueled the rise of “nuclear verdicts” — jury awards exceeding $10 million that were once rare but have now become uncomfortably common. According to industry analysts, these verdicts increased tenfold between 2010 and 2018 in some liability categories.

3. Cases Stretch Into Marathons

Time is typically the enemy of plaintiffs with limited resources. Not anymore.

Without mounting legal bills creating pressure, funded plaintiffs can extend cases indefinitely. Insurance companies must spend more defending each claim, regardless of merit. According to Accenture, the top 50 insurance carriers in 2022 spent an average of $500 million on litigation expenses alone.

That’s half a billion dollars that ultimately comes from one place: your premiums.

4. The Social Inflation Spiral Accelerates

There’s a psychological element too. As outsized verdicts become more common, jurors’ expectations shift. A $1 million award that seemed enormous a decade ago now feels modest by comparison.

It’s like how $20 million used to be a shocking movie star salary, but now barely raises eyebrows. Our sense of “reasonable” compensation has been recalibrated upward.

The Impact Across Insurance Lines

Third-party litigation funding doesn’t affect all insurance equally. Here’s how different coverage areas are feeling the pressure:

- General Liability Insurance: Takes the brunt of product liability and premises liability claims

- Employment Practices Liability Insurance (EPLI): Hit by increasingly expensive workplace claims

- Commercial Auto Insurance: Ground zero for nuclear verdicts in accident cases

- Professional Liability Insurance: Facing more claims and higher settlements

Between 2018 and 2023, litigation management costs across the Property & Casualty industry jumped by 19%, amounting to $4-5 billion. These costs inevitably flow downstream to policyholders through higher premiums.

Why Small Businesses Are Taking the Hardest Hits

When rough waters hit, it’s not the massive cruise ships that suffer most — it’s the small fishing boats.

The same principle applies here. While large corporations can weather increased insurance costs, small businesses often face existential threats from these trends:

- Tighter Financial Margins: Small businesses typically operate with less financial cushion, making premium increases disproportionately painful

- One Case Creates a Premium Earthquake: A single funded lawsuit can cause your premiums to spike for years, even if you ultimately win

- Settlement Pressure Intensifies: Many small businesses feel compelled to settle questionable claims because they can’t afford the uncertainty of extended litigation

- Coverage Options Shrink: As insurers become more cautious, some small businesses struggle to find adequate coverage at any price

The situation is particularly dire in states with plaintiff-friendly legal environments. Florida has become what some industry experts call “ground zero” for extreme litigation. In 2021, six Florida insurance carriers went insolvent despite appearing financially healthy — they were, as one insurance expert put it, “litigated to death.”

Should You Ever Consider Third-Party Litigation Funding?

You might wonder if third-party litigation funding could ever work in your favor. After all, if you can’t beat ’em, join ’em, right?

While there may be rare scenarios where it makes sense — such as when facing a bet-the-company lawsuit against a much larger opponent — approach with extreme caution.

It’s a bit like payday lending. When you’re desperate, the immediate cash seems worth the cost. But the long-term math rarely works in your favor.

Before considering litigation funding:

- Do the Real Math: Funders typically take 30-40% of any recovery, on top of attorney contingency fees, potentially leaving you with a minority share of your own lawsuit

- Understand the Control Issue: Many funding agreements give investors significant influence over settlement decisions, reducing your autonomy

- Explore Alternatives First: Traditional financing, contingency arrangements, or negotiated settlements often provide better outcomes

- Consider the Insurance Aftermath: Using litigation funding could affect your future insurability and premiums

In most cases, businesses are better served by strong risk management practices and maintaining good insurance relationships rather than pursuing funded litigation.

What You Can Do to Protect Your Business

While you can’t single-handedly change the litigation environment, you can build your defenses. Here’s how:

Talk to Your Insurance Agent

Schedule a comprehensive business insurance review with your insurance agent. They can help identify your specific risk exposures and recommend coverage adjustments based on your industry and location. In an era of nuclear verdicts, your agent can assess whether your current liability limits would withstand a worst-case scenario in today’s legal climate. What was considered adequate protection just a few years ago may leave your business vulnerable now.

Strengthen Contracts and Documentation

Think of your contracts as your legal armor. Make sure yours isn’t full of holes.

Review your contracts, waivers, and documentation practices with a fresh eye. Strong contracts with appropriate indemnification clauses, limitation of liability provisions, and mandatory arbitration can help reduce litigation exposure.

The best time to address a potential lawsuit is before it happens, through clear agreements that anticipate modern litigation tactics.

Implement Risk Management Protocols

The cheapest lawsuit is the one that never happens.

Develop and enforce rigorous safety protocols, quality control measures, and employee training programs. Document these efforts meticulously — they’re not just operational best practices, they’re your defense exhibits if litigation strikes.

Consider Umbrella Coverage

Think of umbrella coverage as your insurance policy’s insurance policy.

An umbrella policy provides an additional layer of protection beyond your primary liability policies, often at a relatively affordable rate compared to increasing primary limits. In an era of nuclear verdicts, this extra protection can be the difference between a covered claim and a business-ending event.

Stay Informed Without Becoming Overwhelmed

Understanding the forces affecting your insurance costs empowers better decision-making, but you don’t need to become a legal expert.

Follow industry publications, attend seminars, and most importantly, maintain an open dialogue with your insurance professional. Knowledge isn’t just power — it’s protection.

The Bottom Line: Protect Your Business in a Changing Landscape

Understanding what’s behind your premium increases helps you respond more strategically. While Third-Party Litigation Funding has undoubtedly transformed the insurance landscape, proactive businesses can still find ways to manage their risks effectively.

We’re committed to helping our business clients navigate these challenges. We don’t just sell policies—we provide the expertise and guidance you need to protect your business in an increasingly complex risk environment.

If you’re concerned about how litigation trends might be affecting your coverage or costs, reach out for a comprehensive review of your business insurance program. Together, we can develop a strategy that protects your business without breaking your budget.

Get a Business Insurance Quote

Compare business insurance quotes and rates. We make it fast, safe, and secure.

- Let’s Get Started!

-

Have an Agent Call

Have an Agent Call

- Compare Business Quotes

-

Business Owners’ Policy

-

Workers’ Compensation

-

General Liability

-

Commercial Auto

-

Cyber Liability

- Personal Insurance

-

Auto

-

Home / Condo / Renters

-

Motorcycle

-

Classic Car

-

Boat / Yacht

- Quote & Buy Online

-

Small Business Insurance

-

Mexico Auto Insurance

-

Pet Insurance

Call 1-877-334-7646 to speak with a business specialist

Key Takeaways:

- Hidden cost driver: third-party litigation funding is fueling more lawsuits, larger settlements, and higher business insurance premiums.

- Small businesses hit hardest: rising legal costs and “nuclear verdicts” are driving up rates and shrinking coverage options.

- Protect your business: review liability limits, strengthen contracts, and consider umbrella coverage to stay ahead of social inflation.