Who Really Has the Cheapest Auto Insurance?

Which insurance company has the cheapest auto insurance in California? Does this even matter? One site set out to research this question and provide the definitive answer.

According to Value Penguin, their team of “analysts analyzed cost data to provide drivers in California with information in their search for car insurance quotes and the cheapest companies.”

We reviewed this research, the methodology, and the findings to see if Value Penguin was providing any real value to California auto insurance shoppers. What we found was that the analysis was flawed, the underlying data was not representative of the actual shopping market, and they compared companies that don’t market similar auto insurance products.

While we don’t have a team of analysts here are IronPoint, we are going to attempt to correct the record and hopefully help some consumers who want to understand how to determine if an auto insurance policy is being offered at the right price.

Before we get started, let’s first correct the first statement made by the author, that California auto insurance costs tend to be expensive. Once again, who knows?

Does California actually have high prices for auto insurance?

To fully understand if an entire state’s rates relative to another are “more” expensive, one would first have to normalize the data so that the demographics, weather, medical, and repair costs are all similar. Then you could maybe make a true cost estimate.

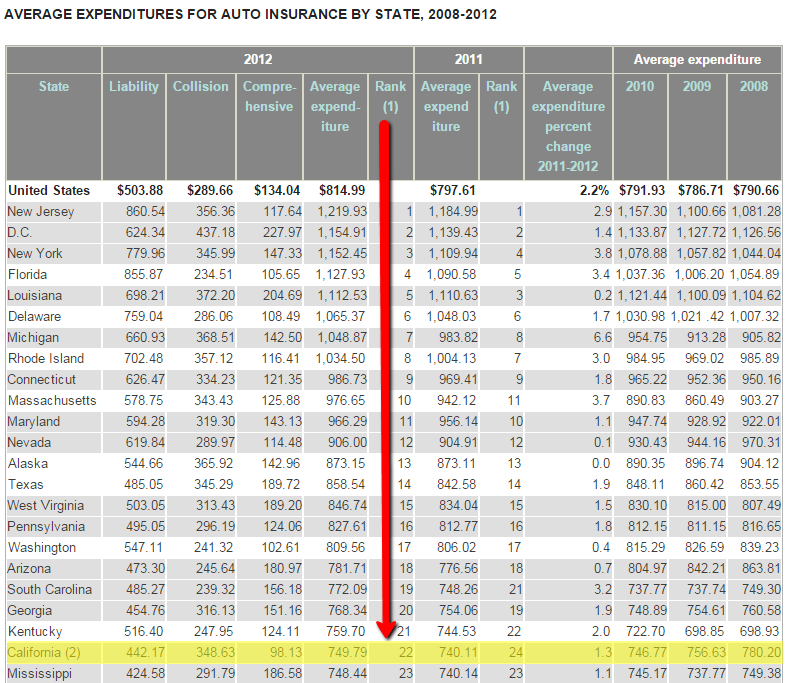

If you just want to know who “pays” more for auto insurance, then that data comes from the National Association of Insurance Commissioners. That data suggests that California ranks 24th in auto insurance expenditure, which makes it average—not among the most expensive.

A few thoughts on the Value Penguin methodology

The Value Penguin article uses data provided by the California Department of Insurance’s annual auto insurance survey. This survey is conducted pursuant to section 12959 of the California Insurance Code, which requires the commissioner to publish and distribute a comparison of insurance rates for personal insurance products of public interest, like auto insurance.

According to the Department of Insurance, the survey “should be used as a guide for consumers in selecting the best premium and coverage.” They further advise that “the premiums displayed in this report are representative of the hypothetical risks used in this study and may not apply to any particular need.”

It’s well understood by the insurance industry that the California auto insurance survey might provide some directional indication of competitiveness for someone who looks like the hypothetical risks, but it lacks the statistical credibility to model the vast combinations of risk characteristics that form the California auto insurance marketplace.

For example, the actual Department of Insurance survey only uses a small number of vehicles in the hypothetical risks, and the Value Penguin study only uses two vehicles, a 2012 Honda CR-V LX and a 2012 Toyota Camry LE.

Some insurance carriers in the Value Penguin study may apply the same rating factor for both of these vehicles; therefore, changing them would provide no difference in rate. Also, if one carrier has classified one of these vehicles in a low premium band, they would continually show up as competitive in the survey results, even as you change zip codes or other rating factors.

This is textbook bias.

Another bias in the Value Penguin analysis is the use of minimum financial responsibility limits. Some of the insurance carriers in the survey actually prefer to sell increased limits, so they get increasingly more competitive as the limits get higher. Comparing Travelers or State Farm for minimum limits in relation to Alliance United simply doesn’t make sense. One only sells minimum limits, and the others sell policies to families who seek increased coverage and likely purchase multiple products.

This leads me to the next level of bias: the survey doesn’t allow for any of the affinity discounts (occupational or otherwise), and it doesn’t account for multi-policy discounts. The multi-line insurance carriers always show their best rates when they apply multi-policy and affinity discounts. Discounts are frequently not offered by some of the carriers that the Value Penguin presents as offering lower premiums.

There is no incentive for the insurance companies to complete these surveys in a way that highlights their most competitive rates. Carriers simply complete the surveys according to the letter of the request, without “options” discounts or the complete application of the underwriting rules. Analyses that rely on this data cannot account for the “street-to-street” rates that are actually provided by insurance agents or raters, where the full application of discounts and rules is applied.

The Value Penguin study doesn’t compare apples to apples

The Value Penguin study has good intentions. The author’s objective is to provide cost analysis for consumers using a reliable statistical framework. Such a study could have some value for consumers if done correctly.

But in the case of this study, along with the bias and poor underlying data, it compares insurance carriers as if they’re all the same. Not all insurance companies are the same, furthering the flaw in the analysis.

Just like in other consumer product or service categories, the insurance sector has its value and premium brands. The value brands offer less coverage, while the premium brands not only offer more coverage, but they typically provide much better customer experiences. It takes an expert, like an insurance agent, to understand these differences sometimes because they reside in the actual policy language … not in the limits of liability or deductibles that are seen on a declarations page.

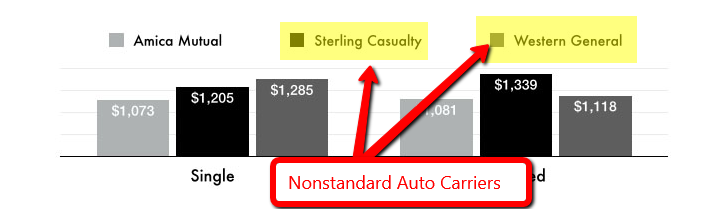

Throughout the study and the breakdowns of the lowest premiums by city, we find comparisons of value brands, typically called nonstandard auto insurance products, to premium brands. In the example provided below, where Value Penguin shares their top three low-cost options for the Los Angeles area, we can see that they predominantly display two nonstandard carriers alongside one premium brand.

In fact, Value Penguin actually states, “if you go with quotes from our five cheapest companies in LA, then rates are about 28% cheaper than the average.” Such a recommendation is irresponsible; securing insurance with Sterling Casualty or Western General, especially if you left Travelers or The Hartford to do so, would represent a huge decrease in coverage, service, and value.

There is a place for nonstandard auto insurance carriers, and they do provide a great service for hard-to-place risks or for consumers who are willing to sacrifice protection and service for savings because monthly budgetary needs take precedence. But to broadly recommend (even if indirectly) considering this type of protection is not prudent, real lives and financial security are at risk.

We reviewed the top ten carriers Value Penguin recommends as the “cheapest auto insurance in California” and 5 of them were nonstandard auto insurance carriers (6 if you include Progressive who got their start in nonstandard auto), two (2) were restricted by membership in a group (Teachers or Military & Government Employment). Only two (2) were broadly available standard auto insurance carriers—Mercury Insurance and Amica Mutual.

Insurance is not a commodity, even if everyone keeps trying to tell you it is

Insurance is one of those things that we don’t consider “sexy.” It’s definitely not like your iPhone, the latest hot HBO Original Series, or social media app. Insurance is a complex financial product that we don’t invest a lot of time in fully understanding. This makes it easy for marketers and bloggers to focus on the simple, easy-to-understand elements—the price and limits of liability.

The system of regulations, statutory reporting to validate financial security of providers, licensing, and continuing education of sales professionals was created because insurance is a serious business—an important element of the macro economy.

Articles like the “Cheapest Auto Insurance in California” don’t consider any of the service, protection, and contractual elements of your auto insurance. It talks of auto insurance as if it’s a cup of coffee. Heck, the author may actually assign more value to a good cup of java than their auto insurance.

With so many articles like these on the internet, it remains the challenge of the insurance agents, tasked with providing protection for our clients, to continue to inform and assist the public why we purchase insurance—to protect the assets that we work so hard to earn.

Conclusion

It’s nice to get feedback about our purchases, especially expensive ones (insurance can be expensive). But you should be very careful when getting information from internet sites about price comparisons. The reality is that price comparisons are hard to do because not all the rates are published, and the department of insurance surveys are not equipped to provide the statistical credibility to conduct accurate evaluations. Some sites will aggregate rates for you, but you still need to understand the policy differences. This is why using an agent is still the very best way to buy insurance, even auto insurance.

Image Source: Daryl Elliott

Let’s Get Started

Select the way you want to start your quote.

Let’s Get In Touch

Compare Quote Online

Let’s Get Started

Want to know if you can save on home or auto insurance? See for yourself. Start a quote today.

Call today and speak with a professional insurance agent.

1-877-334-7646